MEDICARE

Who is Eligible?

Seniors 65+

The majority of our long-term care resources and planning options are designed specifically for individuals aged 65 and older as they transition into retirement.

Disability Support

Coverage and assistance are available for individuals under the age of 65 who are living with qualifying disabilities and require specialized care.

End-Stage Renal Disease

We provide dedicated support for people of all ages suffering from permanent kidney failure requiring dialysis or a transplant (ESRD).

When Do I Enroll?

Most people enroll around their 65th birthday. You can enroll during the 3 months before your birth month, the month of your birth and 3 months after that month giving you a 7 month initial enrollment period. Depending on when you enroll, coverage can start as early as the month of your 65th birthday.

If you miss your Initial Enrollment, you can sign up every year between January 1st and March 31. If you enroll at that time, your coverage is effective July 1st of that year.

Under certain circumstances, you may be eligible for a special Enrollment Period. If you have questions about that, please call me.

If you are still working and covered under employee group insurance you can either enroll in Medicare and drop your group coverage or you may be able to delay enrollment and stay with your employee program. You need to compare your plan at work side by side with your Medicare coverage and decide which is better for you. Before deciding to leave your employer plan, always discuss all of your options with your benefits administrator, insurer, or plan provider. In most cases once you leave, you cannot return to the employer plan.

How Do I Sign Up?

- Enrollment in Medicare is Automatic

- Card arrives in the mail about 3 or 4 months before your 65th birthday

You can start the enrollment process around 100 Days before your 65th birthday.

You can enroll two different ways:

- Call Social Security to

schedule an appointment

800-772-1213 - Sign up at medicare.gov

- Call Social Security to

What Exactly Is Medicare?

The original Medicare program was signed into law on July 30th, 1965. Former President Harry Truman and his wife were the very first beneficiaries. Today over 56 million Americans are enrolled in the Medicare program. That’s most Americans ages 65 and older, regardless of their income or health status.

You’re going to hear a lot about Medicare Supplement policies A through N. Original Medicare has only 2 parts: A and B. Part A is for hospital care and Part B is for medical services. Let’s start there.

Medicare Part A is usually free to you but you have to enroll. Once you do that – you can rely on the basic coverage or purchase supplemental coverage for additional protection.

Part A Hospital Care

Premium Free

- First 60 days covered 100%

- First 20 days of skilled nursing covered 100%

- $1,408 deductible per occurrence*

*for 2020 plans

Medicare Part A is for hospital care. It covers things like your hospital room, meals, general nursing and hospital services and supplies. It does not cover private duty nursing, comfort or convenience items.

Coverage is for up to 90 days per Benefit Period and the first 60 days are covered at 100% after the Medicare Part A Deductible is met. You pay an out of pocket cost for any days after 60. There is an additional 60 days of coverage called lifetime reserve days, but it can only be used once.

It’s important to note that the deductible is $1,408 and applies to any new Benefit Period. So if you go into the hospital for a couple of days, get discharged and then return a week later – you are still in the same Benefit Period and will not be charged again for the $1408 Part A Deductible that you incurred on the first confinement.

If you are out of the hospital and/or Skilled Nursing Facility for at least 60 days in a row, a return to the hospital would begin a new Benefit Period and you would owe the Part A Deductible.

Most people do not pay a premium for Part A.

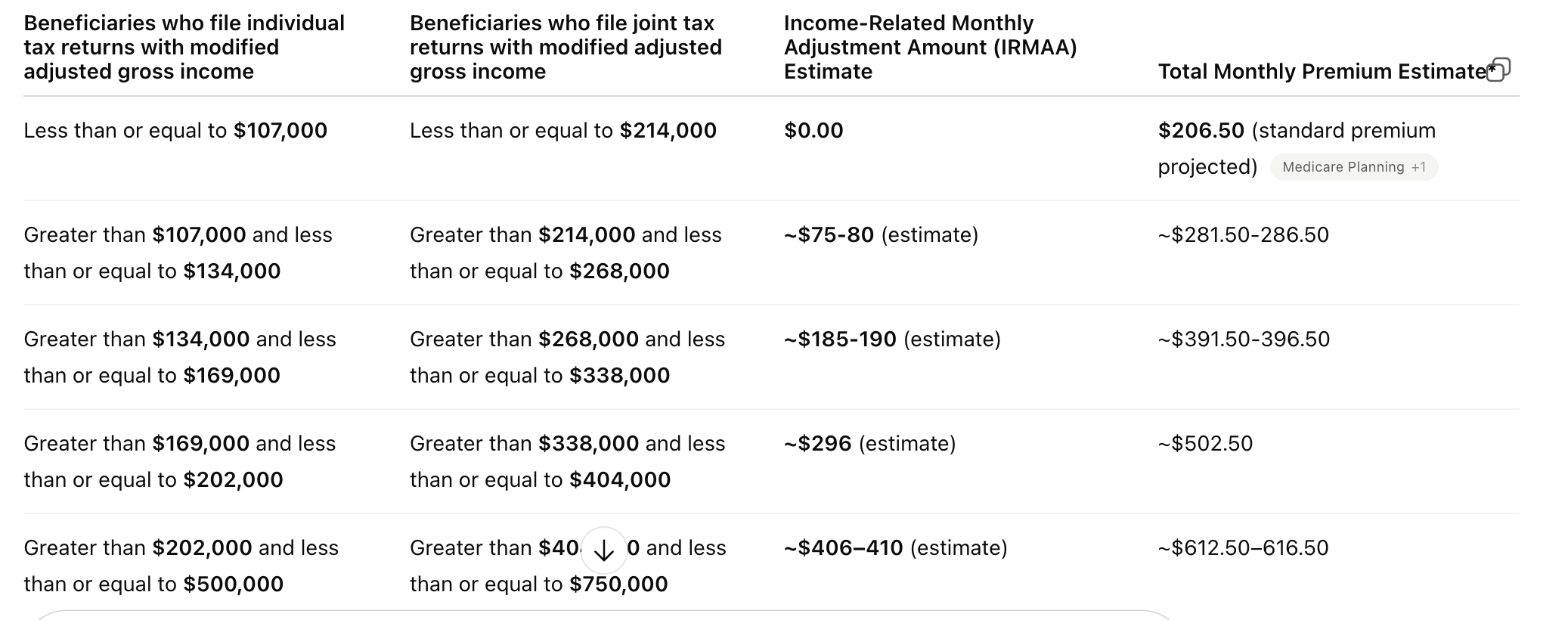

Part B Medical Services

$288 annual deductible

- Covers medical services outside the hospital

- Doctor visits, lab work, x-rays, ambulance, emergency room, outpatient surgery

- An 80-20 plan with Medicare paying 80%

- $288 annual deductible

an increase from $240 in 2024.

This deductible is the amount you must pay out-of-pocket each year before Medicare begins to cover your Part B services. After meeting this deductible, you typically pay 20% of the Medicare-approved amount for most doctor services, outpatient therapy, and durable medical equipment.

What you don’t get with A&B

Original Medicare doesn’t cover

- Dental

- Vision

- Prescription Drugs

- Hearing

- Help with long term care

When you DELAY Part B

If you or your spouse are working you may be able to delay enrolling in Medicare Part B, depending on the size of the employer…

If you are covered under an employer group health plan

You are covered under a spouse’s employer group health plan

- No Penalties

- No loss of Options

Now Where Do You Go…

Do you enroll in Part A, Parts A & B, Medicare Advantage or even a Medicare Supplement plan or do you continue with employer group health coverage or possibly union coverage?

You may also have the option of retiree coverage for health care after you retire but it does not count as creditable coverage for delaying enrollment into Medicare Part B, and neither does COBRA.

Medicare Options & Planning

Retiree or Union Plan

Compare employer or union plans to Medicare A & B. Consult your benefits administrator about:

- Copays and deductibles

- Included drug plans

- Opt-in/Opt-out rules

- Dental and vision coverage

*Note: Retiree coverage is not "creditable" for delaying Medicare Part B.

Medicare Supplement

Standardized Medigap plans (A–N) that cover costs Medicare doesn't. Coverage is identical for the same letter across providers.

- You want to budget fixed costs

- You travel frequently

- You want no referrals for specialists

- You want guaranteed renewability

Medicare Advantage

Part C replaces A & B, often including Part D. These plans use HMO/PPO networks and feature a Maximum Out-of-Pocket limit.

- You prefer lower premiums

- You are a Veteran using VA services

- You like your local doctor network

- You have a low-income subsidy

When you DELAY Part B

- Part D

- Prices vary by county, depending on the plan

- Included with some retirement plans

- Late enrollment penalties may be imposed

- Vets are not required to enroll, but may choose to do so

Financial Assistance & Coverage

Extra Help with Rx

You may qualify for a low-income subsidy to assist with deductibles, co-pays, and premiums if you meet the following criteria:

- Annual Income: Less than $18,735 (Singles) or $25,365 (Couples)

- Resources: Less than $14,390 (Singles) or $28,720 (Couples)

* Amounts based on 2019 data; subject to change in 2020.

2020 Rx Gap

Commonly known as the "Donut Hole," the coverage gap begins after you and your plan spend $4,020.

- Generic: You pay 25%

- Brand-Name: You pay 25% (95% counts toward out-of-pocket)

- Catastrophic: Coverage begins after $6,350

* Thresholds based on 2020 plan limits.

Don't Wait Until Its Too Late

The Right Plan Today Can Protect Your Tomorrow